Northern Trust (NTRS) Rides on Loan Growth, High Costs Ail

Northern Trust Corp. NTRS is well-poised for revenue growth on the back of steady loan demand. The company’s capital distribution activities are backed by a strong liquidity profile. However, rising expenses and weak asset quality remain near-term concerns.

Northern Trust prioritizes organic growth as indicated by an uptrend in revenues and loan balance. Revenues witnessed a compound annual growth rate (CAGR) of 3.5% over the last three years (2020-2023). This was primarily driven by rising non-interest income and net interest income (NII), with some annual volatility. The NII benefited from higher rates and loan balances. Over the same period, the company’s loan and lease balance witnessed a CAGR of 7.7%. The company expects sustained organic growth in the Asset Servicing and Wealth Management segments, primarily due to robust loan pipelines.

The company is focused on expense management efforts to restore its operating leverage over the upcoming quarters. This includes disciplined headcount management, vendor consolidation, rationalization of its real estate footprint and process automation. Through such efforts, the company aims to boost productivity and meet financial targets. The ultimate measure of the success of the company’s past efforts was its ability to consistently achieve a return on equity between 10% and 15%.

As of Dec 31, 2023, Northern Trust’s total debt (comprising long-term debt and other borrowings) was $10.63 billion. Federal Reserve and other Central Bank deposits were pegged at $34.28 billion as of the same date. The higher level of liquid assets compared with the company’s obligations makes the debt levels seem manageable.

Northern Trust’s capital distributions seem impressive. In July 2022, the company hiked its quarterly dividend by 7% to 75 cents per share. Furthermore, the company announced a $25 million share repurchase program with no specified end date. Approximately $980 million was returned to common stockholders, including common stock repurchases of around $350 million in 2023. The company’s favorable debt equity ratio and strong liquidity position will likely support future capital-distribution activities.

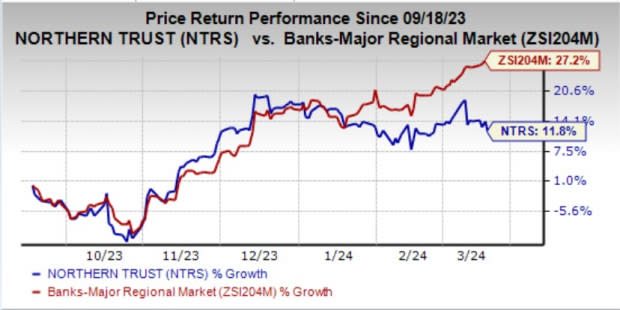

NTRS currently carries a Zacks Rank #3 (Hold). Shares of the company have gained 11.8% over the past six months compared with the industry’s growth of 27.2%.

Image Source: Zacks Investment Research

Despite the above-mentioned tailwinds, the company has been recording a steady rise in expenses. Non-interest expenses witnessed a CAGR of 6.7% over the last three years (2020-2023). Northern Trust’s expenses are likely to remain high on rising compensation and investment in equipment and software expenses. Hence, an increasing expense trend is anticipated to hinder bottom-line growth in the upcoming quarters.

Northern Trust’s credit quality is expected to deteriorate in the upcoming period, given the economic uncertainty. It recorded provision expenses of $24.5 million in 2023 and $12 million in 2022. In 2023, the company also recorded a rise in total non-accrual assets to $65.1 million from $45.9 million in 2022. The worsening economic outlook is expected to keep provisions and non-accrual assets high in the near term, increasing the risk of credit losses.

Stocks to Consider

Some better-ranked bank stocks worth mentioning are The Bank of New York Melon Corp. BK and Bank7 Corp. BSVN.

BK’s earnings estimates for the current year have been revised upward slightly in the past 30 days. The company’s shares have gained 21.5% over the past six months. At present, BK sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Bank7’s 2024 earnings estimates have moved north by 5.8% in the past 60 days. The stock has gained 10.1% over the past six months. Currently, BSVN sports a Zacks Rank #1.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Bank of New York Mellon Corporation (BK) : Free Stock Analysis Report

Northern Trust Corporation (NTRS) : Free Stock Analysis Report

Bank7 Corp. (BSVN) : Free Stock Analysis Report