Bets on Risky CLOs Are Paying Off With 20% Gains: Credit Weekly

(Bloomberg) -- Returns on the riskiest portion of collateralized loan obligations are booming, reaching about 20% annualized on both sides of the Atlantic as loan performance improves, debt spreads tighten and payouts grow.

Most Read from Bloomberg

Xi’s China EV Dream Came True. 10 Years On, Walls Are Going Up

China Creates $47.5 Billion Chip Fund to Back Nation’s Firms

In some cases, a structural quirk that’s allowed managers to put fresh debt on old deals has also aided returns to the equity slice, the first piece of the structure that takes losses. Money managers that put together CLOs — bonds backed by a group of leveraged loans — are taking advantage of falling fundings costs and issuing more lower-rated bonds, instead of hanging onto them.

Many are now selling what’s known as a “deferred class F tranche,” tacking it on to an older CLO. The money they get from the sales can reward equity holders with fresh distributions.

“Managers are able to flush the sale proceeds straight out to equity, which can lead to bumper returns,” said James Baillie, a structured credit partner at Paul Hastings in London.

The deferred tranches are another example of how issuers are taking advantage of a strong rally in risky debt as fears of a recession recede and pricing recovers after a prolonged rocky period. Since the start of the year, more than a dozen such deals have been issued in Europe from CLO managers including Invesco and Capital Four.

Equity returns have also been helped by a number of CLOs exiting their non-call period, meaning they can be refinanced, restarted or liquidated. The new pricing and extended investment timelines can also free up more cash that can be sent to the equity portion, Baillie added.

“In both approaches you’re moving from a less levered to a more levered position and that’s giving you in some instances an equity dividend,” he said.

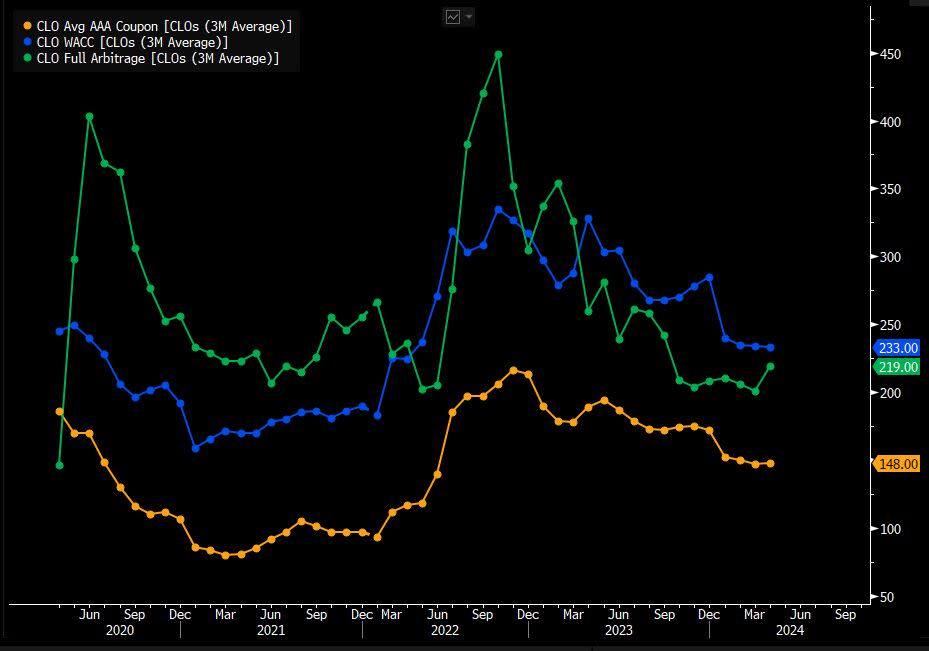

CLO equity returns have been choppy in recent years due to fluctuating arbitrage — or the difference between the yields a manager gets from the loans it buys and the funding costs on the bonds it issues. After falling in 2023, European arbitrage levels have stabilized this year at around 200 basis points, and recently started rising marginally, according to Bloomberg Intelligence.

“In 2022 and 2023, spreads were wider on both assets and liabilities which made placing third party CLO equity more challenging,” Ben Hunsaker, a portfolio manager at Beach Point Capital Management, said of the US market. He said those deals have likely since experienced strong equity payments and should be able to refinance their liabilities when their non-call periods end.

The catch is that these returns might not last. CLO equity investors may see the arbitrage fall again if global central banks begin cutting interest rates this year. An increase in financial distress could also erode returns, though it has remained limited for now.

“The market was pricing in 3% to 4% defaults last year and 4% to 6% defaults this year, but we’ve observed materially less defaults in CLO portfolios, which has benefited CLO equity,” said Dan Ko, a senior principal and portfolio manager at Eagle Point Credit Management.

Click here for a podcast about Invesco buying REITs and bank bonds in credit’s ‘Golden Age’

Week in Review

Credit bulls are pointing at a set of metrics to show that high-grade bonds have rarely been this cheap, burnishing the appeal of corporate debt at a time when it’s offering little upside over government securities.

Investment banks including Goldman Sachs Group Inc. are pitching broadly syndicated refinancings of some of the riskiest types of private credit, in the latest sign that Wall Street is trying to poach back business from direct lenders.

For the first time since the financial crisis, investors in top-rated bonds backed by commercial real estate debt are getting hit with losses.

Robot investors are increasingly taking over credit markets. The shift is pitting investors with technical PhDs against traditional portfolio managers that have business degrees.

United Parcel Service Inc. sold $2.6 billion in high-grade bonds as companies rushed to price new debt ahead of the Memorial Day holiday. Coca-Cola Consolidated Inc. raised $1.2 billion of notes to buy back stock and data center owner Equinix Inc. returned to sell $750 million after scrapping a planned offering in March, following a short-seller attack.

In the high-yield market, Canadian private jet-maker Bombardier Inc. sold $750 million of bonds as it continues to refinance debt.

Alibaba Group Holding Ltd. sold $4.5 billion worth of convertible bonds, a record dollar-denominated sale by an Asian company.

Oak Hill Advisors is leading a roughly $1.4 billion debt package to help finance Advent International’s proposed purchase of a stake in Prometheus Group.

Banks plan to bring a bond sale as soon as next week to help pay for Roark Capital Group’s buyout of restaurant chain Subway.

Peloton Interactive Inc. sold $1 billion in loans, securing more favorable terms after the deal gained traction among investors.

Seafood restaurant chain Red Lobster filed for bankruptcy, succumbing to onerous leases, high labor costs and a disastrous unlimited shrimp promotion.

A lender to beleaguered utility Thames Water is looking to offload about £500 million ($635.5 million) of the company’s loans.

Chinese companies have cut several measures of overseas borrowing to decade or record lows.

China Vanke Co. repackaged some of its privately issued debt into asset-backed securities, a move that effectively allows the builder to push back already deferred payments.

Cerberus Capital Management LP and Intrum AB are in talks to buy a portfolio of about €7 billion ($7.6 billion) in European bad loans.

On the Move

Blackstone Inc. has hired credit veteran Matthew Humphrey for its multi-asset investing team in London, after he spent 11 years at Barclays Plc, ultimately as head of synthetic risk-transfer structuring.

Bobby Jain’s multistrategy hedge fund has tapped Syril Pathmanathan, until recently at D.E. Shaw & Co., to lead the effort to invest in synthetic risk transfers.

Fidelity International halted its European direct lending activities and let go of members of its private markets team.

Barings hired Bob Shettle once again as a managing director. He will join the company’s North America private finance investment committee effective at the end of May.

Bayview Asset Management has recruited Craig Schorr as a managing director in its insurance asset management division. He previously worked at AllianceBernstein, as head of North American insurance.

--With assistance from Amedeo Goria.

Most Read from Bloomberg Businessweek

TikTok Video Playing on Finance Bro Stereotype Becomes a Viral Hit

The Dodgers Mogul and the Indian Infrastructure Giant That Wasn’t

How the ‘Harvard of Trading’ Ruined Thousands of Young People’s Lives

©2024 Bloomberg L.P.