Nordstrom (JWN) Q1 Loss Hurts Stock, Revenues Beat Estimates

Nordstrom, Inc. JWN posted first-quarter fiscal 2024 results, wherein both revenues and earnings surpassed the Zacks Consensus Estimate. The company posted a loss of 24 cents per share against earnings per share of 7 cents in the year-ago quarter. The loss per share was wider than the Zacks Consensus Estimate of a loss of 8 cents.

Total revenues of $3.3 billion rose 5.1% year over year and surpassed the Zacks Consensus Estimate of $3.2 billion. Total company comparable sales (comps) increased 3.8%. The company’s total revenues for the fiscal first quarter included a 75-basis-point (bps) negative impact of the wind-down of Canadian operations. The company’s gross merchandise value ("GMV") increased 4.9%. Sales were aided by growth across both Nordstrom and Nordstrom Rack banners.

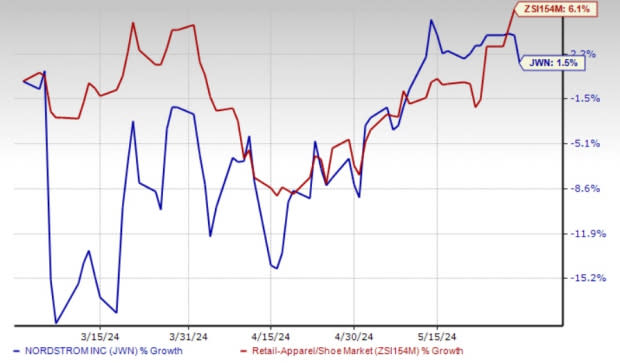

Shares of Nordstrom declined 5.6% in the after-hours trading session on May 30, 2024, on dismal bottom-line performance despite solid sales momentum. Shares of the Zacks Rank #3 (Hold) company have risen 1.5% in the past three months compared with the industry’s 6.1% growth.

Image Source: Zacks Investment Research

Quarterly Highlights

In first-quarter fiscal 2024, the company’s net sales improved 5.1% year over year to $3.2 billion. Credit Card net revenues declined 2.6% year over year to $114 million. Our model predicted net sales growth of 0.3% to $3.07 billion and credit card revenue growth of 0.2% to $117.3 million.

Net sales for the Nordstrom banner rose 0.6% from the year-ago quarter's figure to $2.04 billion in first-quarter fiscal 2024. Comps for the Nordstrom banner rose 1.8% in the quarter. The Nordstrom banner’s net sales included a negative impact of 110 bps related to the wind-down of the Canada operations. The Nordstrom banner’s GMV was flat year over year in the fiscal first quarter. Our model estimated net sales for the Nordstrom banner to decline 1% to $2 billion for the fiscal first quarter.

Sales at the Nordstrom Rack banner advanced 13.8% year over year to $1.2 billion, with comps growth of 7.9%. We expected sales for the Nordstrom Rack banner to improve 3% to $1.1 billion for the fiscal first quarter.

Digital sales fell 0.2% year over year in the fiscal first quarter, accounting for 34% of quarterly net sales. First-quarter fiscal 2024 represented the fourth straight quarter of sequential improvement in digital sales.

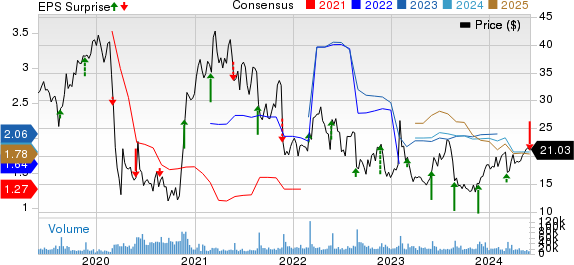

Nordstrom, Inc. Price, Consensus and EPS Surprise

Nordstrom, Inc. price-consensus-eps-surprise-chart | Nordstrom, Inc. Quote

Nordstrom's gross profit margin contracted 225 bps year over year to 31.6% in the reported quarter mainly due to the timing matters related to both higher loyalty activity and reserves, external theft in its transportation network and inventory cleanup in its supply chain due to consolidation of facilities. This was partly negated by top-line growth in the quarter. The company’s gross margin was below our estimate of 35.8% for the fiscal first quarter, a decline of 40 bps.

SG&A expenses, as a percentage of sales, declined 20 bps year over year to 35.8% due to leverage on higher sales and improvement in variable costs in the supply chain and across the business. This was partially offset by higher labor costs. In dollar terms, SG&A expenses increased 4.5% year over year to $1.2 billion. Our model predicted an SG&A rate of 35.3% for the fiscal first quarter, up 60 bps year over year.

Backed by the gross margin contraction and elevated SG&A expense rate, the company reported a loss before interest and taxes of $21 million compared with $259 million in the prior-year quarter.

Other Financials

Nordstrom ended first-quarter fiscal 2024 with available liquidity of $1.2 billion, including $428 million of cash and cash equivalents. The company retired $250 million notes in April using cash on hand, which strengthened its financial position. It had a long-term debt (net of current liabilities) of $2.6 billion and total shareholders’ equity of $836 million as of May 4, 2024.

As of May 4, 2024, JWN’s net cash provided for operating activities was $139 million. The company spent $91 million on capital expenditure in the fiscal first quarter. Nordstrom recently approved a dividend of 19 cents per share, payable Jun 19, to shareholders of record as of Jun 4.

Outlook

Management reaffirmed its guidance for fiscal 2024 on continued revenue strength as displayed in the fiscal first quarter. Additionally, the company noted that the gross margin-related timing issues were addressed through prompt actions.

For fiscal 2024, JWN expects total revenues, including retail sales and credit card revenues, between a decline of 2% and an increase of 1%. Revenues for fiscal 2024 are likely to include a headwind of 135 bps from the additional 53rd week in fiscal 2023. It expects fiscal 2024 comps between a 1% year-over-year decline and a 2% increase.

Additionally, the company warned of quarterly cadence for revenues. It expects second-quarter fiscal 2024 revenues to benefit from a 200-bps gain related to the timing shift of its anniversary sale this year, which is expected to have one day fall into the third quarter of this fiscal year compared with eight days in third-quarter fiscal 2023.

JWN projects an EBIT margin of 3.5-4% for fiscal 2024. It expects an effective tax rate of 27% for fiscal 2024. Nordstrom envisions earnings per share of $1.65-$2.05, excluding any share repurchase impacts. The company expects capital expenditure of 3-4% of net sales for fiscal 2024.

Stocks to Consider

We have highlighted three better-ranked stocks, namely Abercrombie & Fitch Co. ANF, Levi Strauss & Co. LEVI and J.Jill JILL.

Abercrombie, a specialty retailer of premium, high-quality casual apparel for men, women and kids, currently flaunts a Zacks Rank #1 (Strong Buy). The company has a trailing four-quarter earnings surprise of 210.3%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Abercrombie’s current financial-year earnings per share suggests growth of 24.2% from the year-ago reported figure.

Levi Strauss, which designs and markets jeans, casual wear and related accessories for men, women and children, presently carries a Zacks Rank of 2 (Buy). The company has a trailing four-quarter earnings surprise of 16.4%, on average.

The Zacks Consensus Estimate for Levi Strauss’ current financial-year sales and earnings suggests growth of 2.9% and 15.5%, respectively, from the year-ago reported figures.

J.Jill operates as a specialty retailer of women’s apparel. It currently carries a Zacks Rank of 2. JILL has a trailing four-quarter earnings surprise of 621.6%, on average.

The Zacks Consensus Estimate for J.Jill’s current financial-year sales and earnings suggests growth of 1.7% and 8%, respectively, from the year-ago reported figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Nordstrom, Inc. (JWN) : Free Stock Analysis Report

J.Jill, Inc. (JILL) : Free Stock Analysis Report

Levi Strauss & Co. (LEVI) : Free Stock Analysis Report