ConocoPhillips: Bigger Is Not Always Better

Houston-based energy giant ConocoPhillips (NYSE:COP) released its first-quarter 2024 results on May 2. The company is one of the world's largest independent oil and gas producers, with the lower 48 accounting for 55% of oil equivalent production, particularly in the three most productive basins: Permian, Eagle Ford and Bakken.

ConocoPhillips reported adjusted earnings per share of $2.03 in the first quarter of 2024, which exceeded analyst expectations.

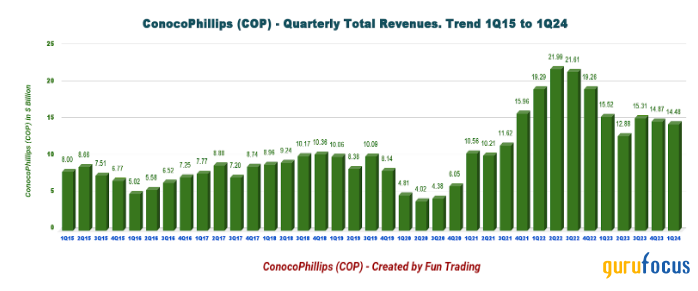

It represents an increase from the adjusted profit of $2.38 per share a year ago. ConocoPhillips' first-quarter revenue was $14.47 billion, down from $15.52 billion the previous year. The company paid a dividend of 78 cents per share and purchased $1.30 billion in stock this quarter. The dividends comprised ordinary dividends and VROC payments.

During the quarter, the company produced 1,902,000 barrels of oil equivalent per day, up 6.10% from 1,792,000 Boepd in the previous quarter.

Image from COP Presentation

CEO Ryan Lance noted in the conference call:

"It was a solid start to the year. We are on track with the full-year guidance that we laid out back in February, which anticipates a well-balanced growth across our global portfolio."

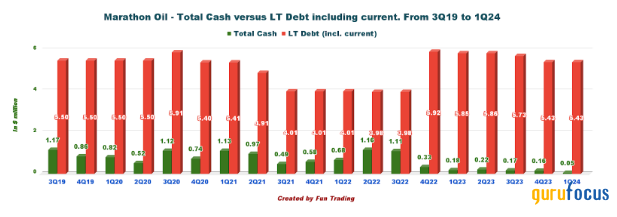

However, the primary focus of this analysis is the recently announced merger of ConocoPhillips and Marathon Oil (NYSE:MRO). It is an all-stock transaction worth approximately $22.50 billion, including net debt. As of the first quarter, Marathon had $5.43 billion in long-term debt, including current and cash of $49 million.

The question for shareholders is whether it is relevant and will provide a tangible benefit.

One significant benefit of the transaction is that it immediately increases cash flow and earnings while adding developed and operational wells to inventory without requiring ConocoPhillips to invest additional capital in drilling new wells.

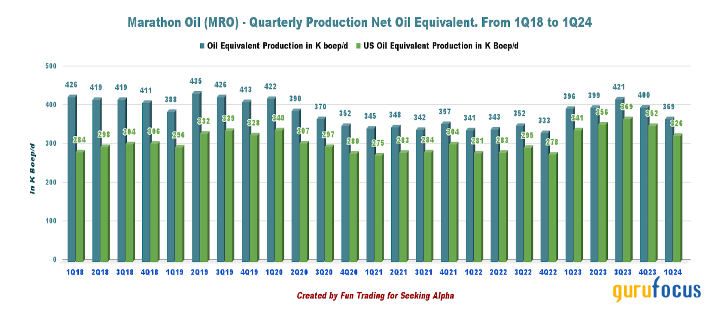

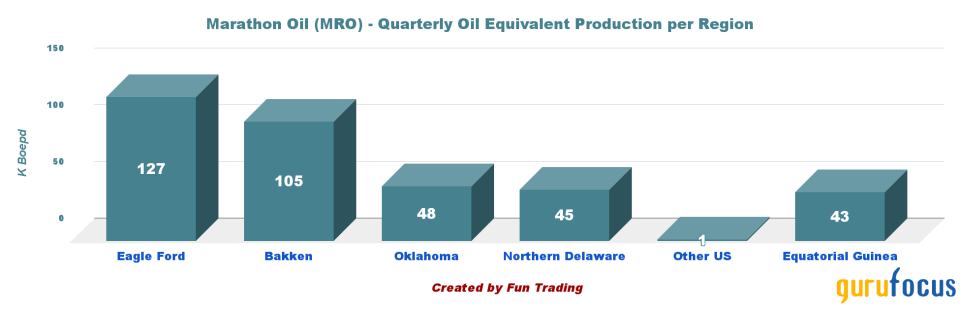

The idea is to grow through acquisitions instead of organically. Marathon Oil's oil equivalent production was 369,000 Boepd in the first quarter, down from 396,000 Boepd in the prior-year period. The chart below indicates its production history.

Marathon Oil's production is concentrated in the U.S., with only a small production in Equatorial Guinea. Below are the details for the first quarter.

The new ConocoPhillips will be larger with a market capitalization of more than $150 billion and will strengthen its position as the world's leading independent oil and gas producer.

As shown above, the company will add production to the Eagle Ford, Bakken and Permian basins. It will also add production to the Oklahoma Basin and Equatorial Guinea, West Africa. Oil equivalent production combined was 2,271,000 Boepd in the first quarter with revenue of $1.60 billion.

However, these benefits may not benefit current ConocoPhilips shareholders, and it is unclear whether shareholders will ever receive a bonus due to this transformation. I doubt it, and I believe it may have a negative long-term impact on dividends. Time will tell, as it always does.

Why do I believe bigger is not always better in the oil business?

Oil analysts increasingly believe an oil company's size no longer guarantees long-term profitability. If current trends serve as any indication, a combination of operating costs, industry specifics and market potential may be increasingly working against the larger companies. Above all, oil prices are extremely volatile, so acquiring a company based on potentially elevated commodity prices can turn such a merger into a fiasco despite its initial appeal.

For the past fifty years, oil majors and large exploration and production companies such as ConocoPhillips have sought to establish dominance through acquisitions. It worked well for the oil patch (Permian, Bakken and other U.S. basins) at first, but now we are dealing with mature basins that are about to decline or are already declining.

This attitude has resulted in numerous cycles of acquisitions and mergers, with somewhat disappointing results for investors despite the potential for synergies and cost savings estimated at $500 million within five years in the case of Marathon Oil's recent merger.

Simply put, the production-to-cost ratio does not provide a sufficient profit margin to significantly impact the new company's stock price. The size of the volume extracted is also important. Despite a $22.50 billion price tag and a more than $5 billion increase in net debt, oil equivalent production is not particularly appealing.

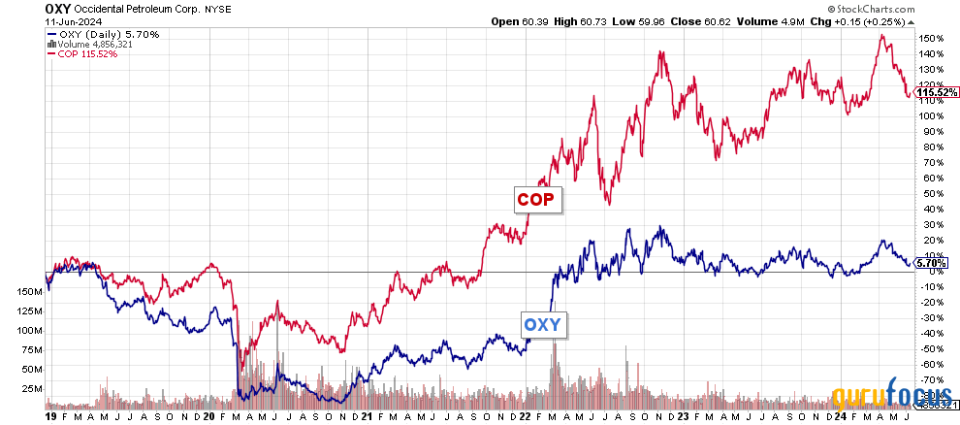

Consider what Occidental Petroleum (NYSE:OXY) did with Anardako in August 2019. A $38 billion acquisition has caused controversy. Shareholders were shortchanged and lost a significant amount of money in the process. The stock has barely recovered to its 2019 valuation, and dividends remain significantly lower despite a significant production increase.

ConocoPhillips is down to approximately 13% year over year, while Marathon is up 22% after underperforming the stock until recently.

Analysis: Balance sheet and upstream production

ConocoPhillips reported total revenue of $14.47 billion for the first quarter, a decrease from $15.52 billion in the same quarter last year. Net income was $2.55 billion, or $2.15 per diluted share, compared to $2.92 billion the previous year, or $2.38 per diluted share.

The company's first-quarter total expenses fell slightly to $10.67 billion from $10.95 billion in 2023. The lower-than-expected quarterly earnings were due to lower commodity prices, partially offset by record oil equivalent production of 1,902,000 boepd.

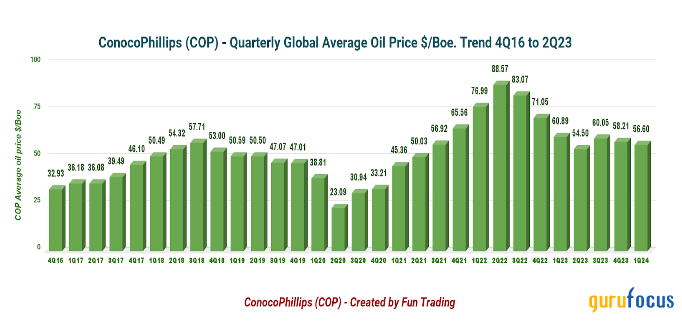

Capital expenditures came out to $2.91 billion, up from $2.89 billion a year ago. The first-quarter cash flow from operations was $4.98 billion at an average oil price of $56.60 per boe.

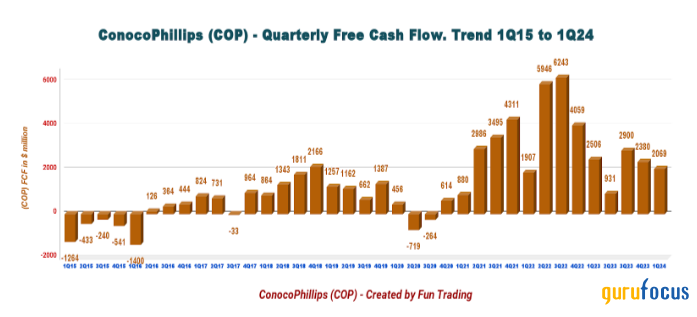

Free cash flow

Free cash flow is an excellent indicator of financial well-being, as it represents the company's ability to generate cash after accounting for capital expenditures necessary to maintain or expand its asset base.

The cash is available to the company to pay dividends and buybacks without issue. The free cash flow on a yearly basis is now $8.28 billion, while dividend costs are less than $1 billion per year, which means the company is not paying an adequate dividend with a current yield of 2.80%.

Free cash flow was $2.07 billion, compared to $2.51 billion in the prior-year period.

Oil production

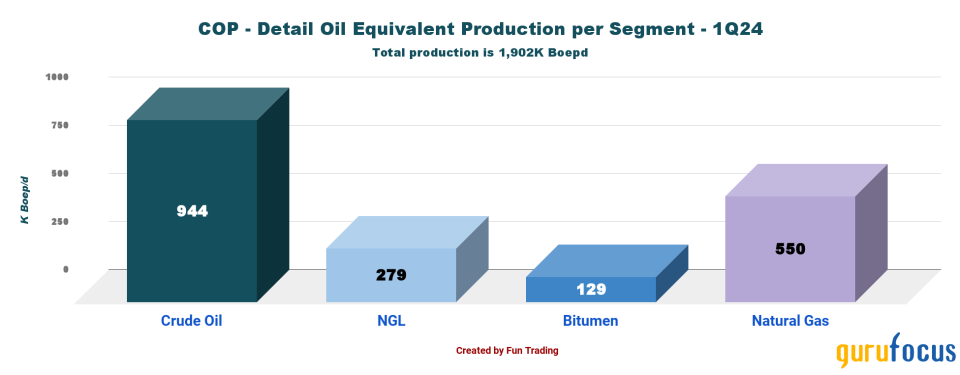

Production for the quarter was 1,902,000 Boepd, up from 1,792,000 Boepd in the same quarter a year ago.

Of the total output, 49.60% was crude oil. Production this quarter represented 2% underlying growth.

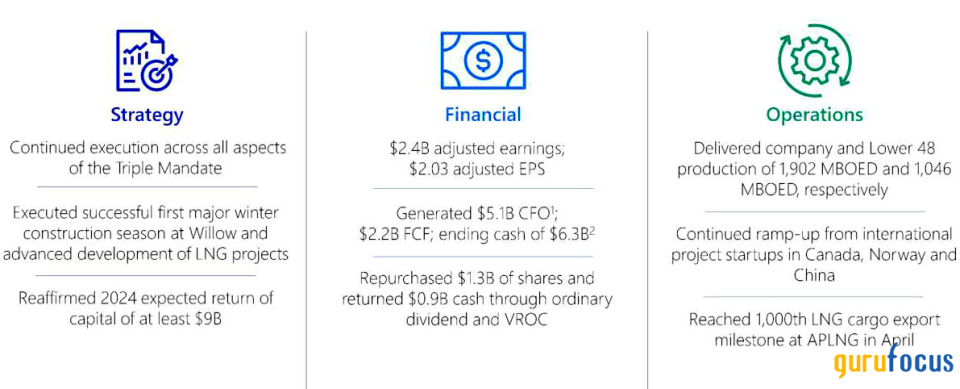

Note, second-quarter 2024 production is expected to be 1,910,000 to 1,950,000 Boepd. The full outlook from the company's presentation is attached below.

Source: COP Presentation

Details per commodity: 51.6% was crude oil

The global average oil equivalent price was stable yearly, from $60.89 last year to $56.60.

The average crude oil price for the first quarter was $78.64 per barrel, slightly up from the year-ago realization of $77.65.

The realized price of natural gas liquids was $24.25 per barrel, up from the year-ago quarter's $25.84.

The average natural gas price for second-quarter 2023 was $5.02 per thousand cubic feet, down from the year-ago period's $7.30.

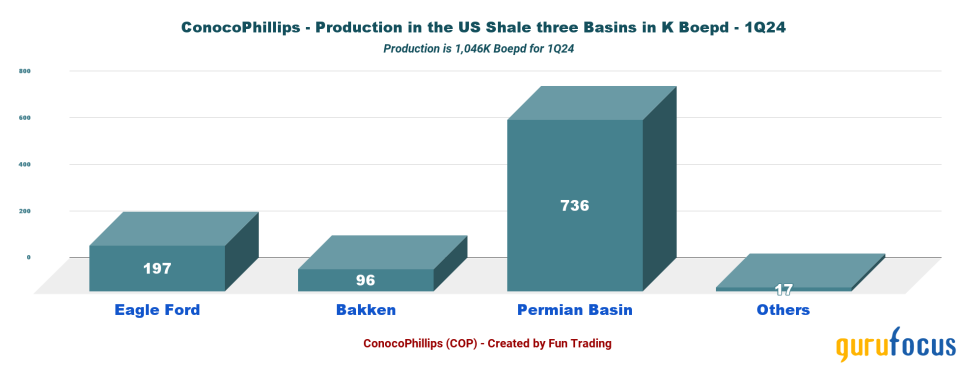

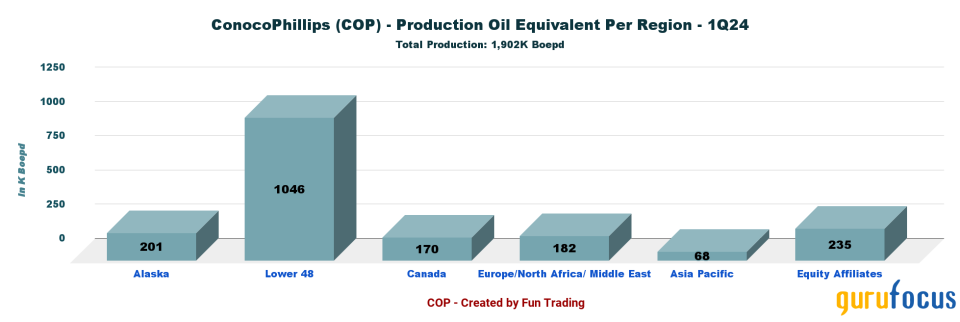

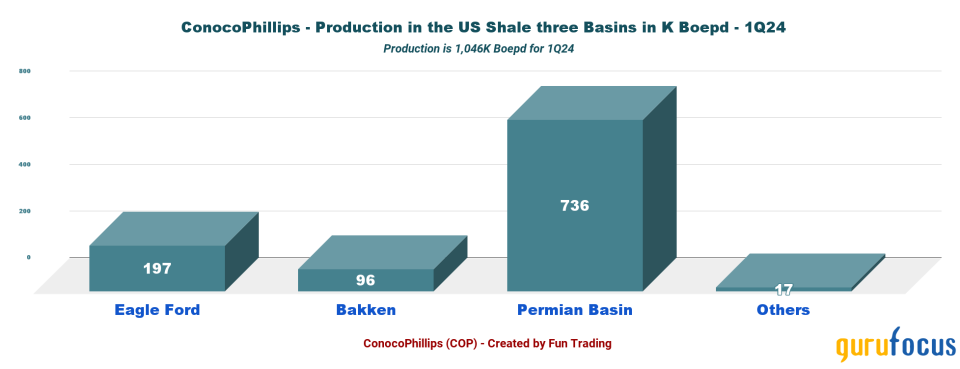

Production in Boepd per region. The Lower 48 is the most significant part, with 55.1%.

Production in the Lower 48 represents 55.10%, or 1,048,000 Boepd, of the total output. The Lower 48 comprises the three U.S. shale basins (Eagle Ford, Bakken and Permian Basin) and the Gulf of Mexico production, but not Alaska.

However, the production of the three basins was 1,029,000 barrels per day.

The Permian Basin is the most prolific for the company and represents 38.70% of the company's total output.

Chief Financial Officer William Bullock said in the conference call:

"Lower 48 production averaged 1,046,000 barrels of oil equivalent per day, with 736,000 in the Permian, 197,000 in the Eagle Ford and 96,000 in the Bakken. Now this included a 25,000 barrel per day headwind from weather, which impacted Lower 48 production by about 2% and was slightly higher than the 20,000 barrel per day guidance provided on the fourth quarter call."

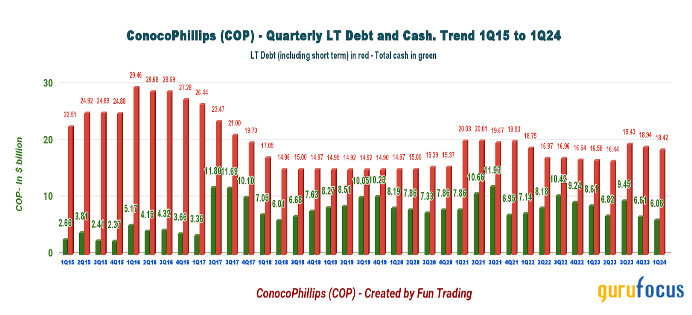

Net debt is approximately $12.35 billion, with $6.06 billion in cash, cash equivalents and securities. After the merger is completed with Marathon Oil, the net debt will jump to $17.74 billion.

Technical analysis and commentary

Note that the chart has been adjusted to account for the dividend.

ConocoPhillips is in a descending triangle pattern, with resistance at $117.5 and support at $111. A relative strength index of 27 indicates an oversold situation, implying a buying opportunity.

However, depending on oil and gas prices, we may break down support and reach below $105.

Descending triangle patterns are typically bearish, but in rare cases, they can be bullish if oil turns bullish, which is less likely.

The mid-term oil and natural gas projection is difficult to determine, but I am less optimistic.

Thus, I believe that selling 30% yo 40% (trading LIFO) between $116.7 and $120 with potential higher resistance at $124.75 or waiting to buy between $112 and $108.20 with potential lower support at $105 to consider adding again is a sound winning strategy here.

Warning: The TA chart must be updated frequently to be relevant.

This article first appeared on GuruFocus.